Reducing Global Warming In the Most Cost-Effective Way

A shift of the tax burden from other taxes to the causes of global warming, such as fossil fuels, that does not change the total tax revenue or the degree of progressivity of the total tax system.

An end to regulations, subsidies and tax advantages that promote the use of alternative “green” products and practices that reduce global warming (such as electric cars, wind energy or solar energy) and and end to regulations, subsidies and tax advantages to promote the fossil fuel industry.

The word “shift” above is very deliberate. It is meant to accomplish these three objectives: (1) isolate the issue of policies to reduce global warming from the issue of the total level of taxation or how progressive it should be, (2) assure the public that this is not a means to raise taxes and (3) prevent the solution to the global warming problem from becoming an excuse to raise taxes.

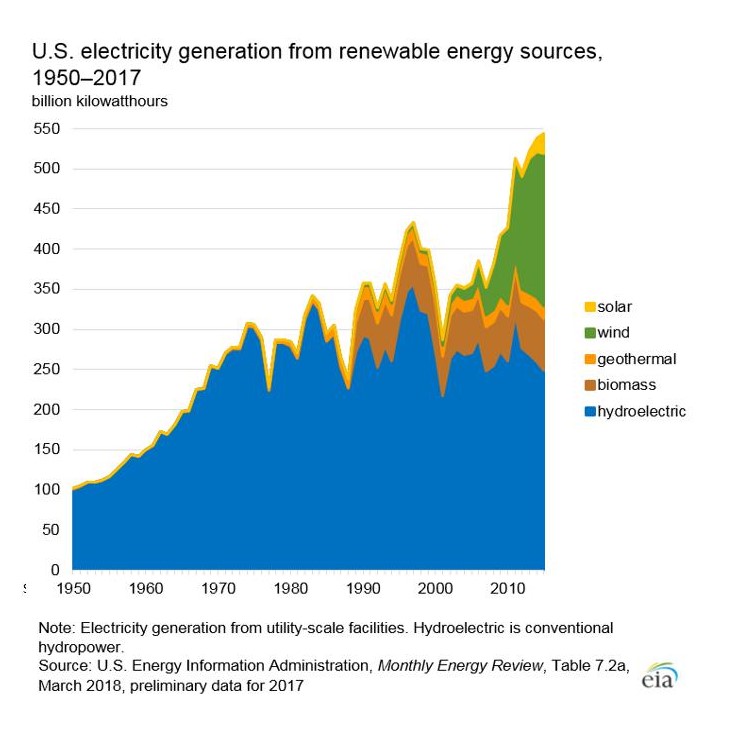

This specific proposal concentrates on CO2, produced by burning coal oil and natural gas, because it has by far the largest impact on Global warming of all the gases generated by human activity: 82%. It is also where the use of a sales tax would be most effective and least costly to administer. See Figure 11 from the federal Environmental Protection Agency and Figures 12 and 13 from the US Energy Information Administration.

Figure 11

Figure 12

Figure 13

The three other types of gasses on Figure 11: (1) are contributing much less to global warming than CO2 and (2) cannot all be as easily reduced using only a sales tax. An example of (2) is the escape of natural gas (methane or CH4) through leaks in their pipelines. It is a small amount in pounds, but its global warming effect per pound is 86 times greater over 20 years and 34 times greater over 100 years then that of CO2, according to Scientific American. This extra amount of greenhouse effect due to escaping, rather than burning, natural gas would not be covered by the tax on its use as a fuel. It would have to be dealt by regulations with heavy monetary penalties for leaks to incentivize gas pipeline companies to do a better job of preventing them.

The relative tax rate of this fossil fuel tax would be in direct proportion to pounds of CO2 emitted per million British thermal units (BTU) of energy, as shown on Table 1. The absolute level of these tax rates should be based on making their total tax revenue equal to the total amount of environmental costs of these fossil fuels. The determination of that total tax level is quite complex and uncertain and estimating it requires resources beyond what I have available. Therefore, that is beyond the scope of this article.

And, in practice: (1) there has to be a consensus in favor of this tax shifting plan before we need to determine how much of total tax revenue should be shifted to fossil fuels and (2) to minimize economic disruption, it should start low and be gradually increased over several years, so we have those years to learn about its effect and refine how high it should end up at.

I suspect that a tax on fossil fuels is likely to be somewhat regressive (because people with higher incomes probably spend a lower percent of it on fossil fuels). If this is true, to prevent a change in the progressivity of total taxes, the income tax rates would have to be increased at higher incomes and reduced at lower incomes by appropriate amounts.

This taxation shift proposal and the arguments for it are far from new or original. I am writing about it as an effort to expose it to more people, since it gets very little attention in the popular media. Instead, the media pays a disproportionate amount of attention to the “sexy” subject of electric cars.

Proposals to tax fossil fuels are typically known as a “carbon tax” or “putting a price on carbon” because the most important of several elements in fossil fuels is carbon, by itself, or as a compound with hydrogen, or other elements, mostly of organic origin. Or it could also be called a tax on fossil fuels. I call my specific proposal “a shift in taxation to fossil fuels”.

The idea of taxing fossil fuels to fight global warming is the favorite of most economists because of its much greater impact on reducing global warming in relation to its costs than other practices or proposals on this subject. See Brookings, The Tax Favored by Most Economists and from Institute for Policy Integrity, New York University School of Law, Expert Consensus on the Economics of Climate Change: “The vast majority (75%) of respondents believe that the most economically efficient way for states to comply with the U.S. Environmental Protection Agency’s “Clean Power Plan” carbon regulations is through “market-based mechanisms coordinated at a regional or national level (such as a regional/national trading program or carbon tax).”

The reference to “a regional/national trading program” above is more specifically the “cap and trade” system. In cap and trade, the government sets a cap to the number of tons of a gas, such as CO2, that can be emitted by industries. Then it offers emissions quotas of tons in an auction that total the tons of the cap. The affected companies have to limit their emissions to the extent of the emission quotas they bought. The smaller the amount of the total cap, the more expensive the emission quotas become. But some cap and trade systems give away all or part of the quotas to the companies. The cap quotas can be traded among the companies. This system gives them an incentive to find ways to limit their emissions. This is already in use in Europe, three state regional compacts in the US and a few other places.

There are several reasons why I believe that the tax-shift approach is superior to cap and trade. If there is an interest on the cap and trade subject in the comments I will write another article explaining the reasons.